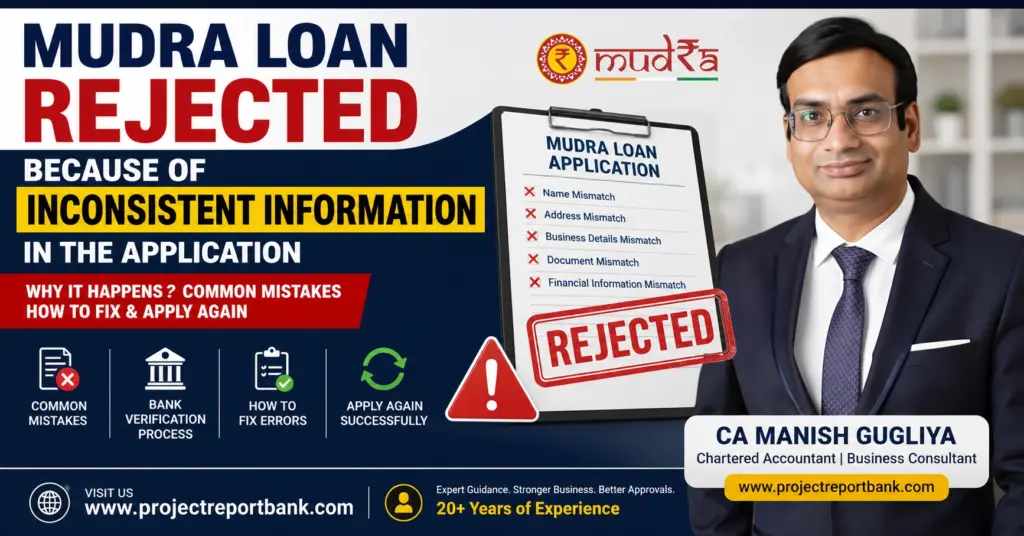

Many entrepreneurs believe that submitting all required documents guarantees a mudra loan approval. In reality, banks compare every detail across your application form, Aadhaar, PAN, bank statements, GST records, Udyam Registration and project report. Even small discrepancies can raise doubts, leading to your mudra loan rejected due to incorrect information. This article explains exactly why this happens and how to fix it before reapplying.

Key Takeaways

- Incorrect or inconsistent information is a common reason for loan rejection, even when the business itself is strong. Incomplete or mismatched documents cause most Mudra loan rejections.

- Applications can fail due to small discrepancies in personal details – a name spelling difference between Aadhaar and PAN, a different address on your rental agreement, or mismatched business start dates across Udyam and the mudra loan application.

- You can usually correct these mistakes by aligning documents, updating government records, revising the project report and submitting a clean application.

- Banks cross-check data through PAN, Aadhaar, cibil score, GST, Udyam and field inspection. Guesswork or copying old details leads to data mismatch and suspicion of an unjustified loan.

- As a practising CA and MSME consultant, I will explain step-by-step how to identify inconsistencies, fix them and reapply confidently for the right loan amount and business loan category.

Consider a common scenario: in 2024, an applicant applied for a Kishore category mudra loan of ₹3.5 lakh for a tailoring unit. Every document was submitted. Yet the bank rejected the application – not because the business was weak, but because the information across documents did not match.

This happens because banks under Pradhan Mantri Mudra Yojana do more than collect paperwork. They verify every line against Aadhaar, PAN, bank statements, GST returns, Udyam Registration, utility bill records and the project report. When India launched the PMMY scheme, the intent was to support micro entrepreneurs in non-farm, non-corporate income-generating activities, but lender institutions still assess risk carefully.

Mudra loans have four categories: Shishu loans are up to ₹50,000 for new businesses, Kishore loans range from ₹50,001 to ₹5 lakh, Tarun loans are available from ₹5,00,001 to ₹10 lakh, and Tarun Plus loans offer up to ₹20 lakh for repeat borrowers. As the amount increases, documentation scrutiny gets stricter. Mudra loans are available for amounts up to ₹20 lakh, and many applicants underestimate how thoroughly banks – including regional rural banks, SBI, Canara Bank and others – verify every detail.

This article focuses specifically on rejections caused by inconsistent information, not on other reasons for Mudra loan rejection like previous loan defaults.

Table of Contents

What Does “Inconsistent Information” Mean in a Mudra Loan Application?

Inconsistent information means the same fact – your name, address, business details, income or loan purpose – appears differently across different documents or systems. KYC mismatches include spelling differences or address mismatches between documents. Even unintentional errors count.

Identity mismatches: Your Aadhaar says “Sunita Devi Verma” but PAN reads “Sunita D. Verma.” Father’s name has a slight variation. Date of birth differs by one digit. Different mobile numbers appear on the form and bank records.

Address mismatches: Aadhaar shows your village address, the mudra loan application lists your rented shop in town, and your business address proof on GST registration shows a third location entirely.

Business mismatches: Business name written differently in the application versus Udyam certificate. GST registration says “trading” but the project report describes manufacturing. Business commencement date in your shop licence says April 2022, but Udyam registration shows 2024.

Financial mismatches: Turnover claimed in the form or business plan is ₹24 lakh annually, but bank statements show only ₹7 lakh in credits. Profit figures differ from ITR. The loan amount requested does not align with investment mentioned in the project report.

Even using a nickname, copying an old address or estimating turnover without checking records qualifies as incorrect information in loan application processing.

How Banks Actually Verify Your Mudra Loan Application

From a banker’s perspective, mudra loans may be collateral-free but are not risk-free. Data consistency is their first line of defence. Banks do not provide direct loans without verification, and no institution offers direct loans based on paperwork alone.

Internal checks: The branch scrutinizes form completeness, verifies KYC (matching Aadhaar, PAN, photographs), checks existing customer details, previous loans and credit history. A CIBIL score above 700 is preferred for Mudra loans, while a CIBIL score below 650 often leads to loan rejection. The bank reviews your cibil report and transaction history for regular transactions.

External verifications: PAN and Aadhaar validation happens through UIDAI and NSDL portals. GST registration and returns are cross-checked. Udyam Registration is verified through the government portal. Banks require proof of ongoing business operations for loan approval – applicants must provide proof of ongoing business operations.

Field inspection: For Kishore and Tarun category loans above ₹2–3 lakh, a banker typically visits the business premises to verify that location, activity, machinery and stock match what is written. If what they see contradicts your project report, the application fails.

Financial consistency: The bank reviews your repayment capacity by comparing the project report, CMA data and bank statements. They assess whether the EMI for the requested loan fits realistically with observed cash flow and your repayment plan. Most banks evaluate business viability at their sole discretion.

Every mismatch increases perceived credit risk, and a seemingly minor error becomes grounds for mudra loan rejected after document verification.

Real-Life Style Examples of Mudra Loan Rejection Due to Incorrect Information

Based on my experience handling mudra loan applications across multiple states, here are common patterns:

Example A – Name and address mismatch: An applicant’s Aadhaar shows “Ramesh Kumar Yadav” with a village address. PAN reads “Ramesh K. Yadav” with a town address. The loan form uses “Ramesh Yadav” with a rented shop address. The bank cannot confirm all three belong to one person. Candidates should ensure that KYC documents match perfectly across ID proofs. Fix: update Aadhaar spelling and address, use consistent name everywhere.

Example B – Investment mismatch: A project report shows ₹12 lakh total cost with ₹8 lakh term loan needed. But the form requests ₹10 lakh. The bank suspects over-financing. Applying for an unjustified loan amount can result in rejection. Fix: align the project report figures exactly with the application.

Example C – Activity mismatch: Application says manufacturing (started 2022). GST shows trading (registered 2024). Udyam says “service sector.” The banker cannot determine the true business model. Fix: update all registrations to reflect the actual activity consistently.

Example D – Income vs bank statement mismatch: The simple business plan claims ₹2,00,000 monthly sales, but six months of bank statements show average credits of only ₹60,000. Insufficient bank account activity signals financial instability to lenders. Fix: base projections on actual evidence, route sales through the bank account, and adjust the loan amount to match reality.

Documents and Details That Must Always Match for Mudra Loans

Before submitting any mudra loan application – especially for Kishore and Tarun category loans – use this checklist to verify consistency:

Identity & Address:

- Aadhaar, PAN, voter ID, driving licence – name, father’s name, date of birth must be identical

- Latest electricity bill or utility bill, registered rental agreement, property tax receipt – current address must match the application

- Udyam Registration is recommended for Mudra loan applicants and should reflect your correct business address

Business Documents:

- Udyam Registration, GST registration, shop licence, business registration – business name, constitution (proprietorship, partnership), and address must align

- FSSAI (food businesses), professional tax, partnership deed if applicable

Financial & Banking:

- Last 6–12 months’ bank statements from your current account – turnover visible here must support what you claim

- Latest ITR, balance sheet, profit & loss account, existing loan statements, cibil report

- Ensure revenue figures and income match across all documents

Project & Asset Documents:

- Project report, CMA data, machinery quotations (dated within 3–6 months), proforma invoices

- Investment amount, loan amount, purpose and clear business plan figures must be internally consistent

Applicants should verify that all documents are consistent before submission. Treat this as a step-by-step checklist to tick off before signing the form.

How to Review and Correct Your Mudra Loan Application Before (Re)Submitting

Even if your first application was rejected, treat it as a draft. Corrections to inaccuracies in the application must be submitted before reapplying.

Personal details checklist: Verify your full name, father’s/spouse’s name, date of birth, Aadhaar number, PAN number, mobile number and email ID. Every field must exactly match your KYC documents and existing bank account records.

Business data checklist: Cross-check business name, constitution, business address including PIN code, date of commencement, nature of activity (trading, manufacturing, services), employee count, GST and Udyam registration numbers. These should say the same thing everywhere.

Financial checklist: Compare last year’s turnover against what the mudra loan application states. Check net profit versus EMI capacity. Verify total existing loans versus debt mentioned. Confirm how working capital and term loan components are split. Ensure cash sales figures reasonably match bank deposits.

Project report review: Read the entire project report line by line. Ensure all numbers, machinery brand names, locations and promoter contribution figures match the bank form. Simply editing the first page without updating annexures is a frequent mistake that leads to mismatched documents.

Before resubmission, either take professional help or have a trusted person review the complete set focusing only on consistency.

Step-by-Step Action Plan If Your Mudra Loan Is Already Rejected

A mudra loan rejection due to inconsistent information is usually repairable. It does not permanently block you from getting finance.

Step 1 – Get the real reason: Lenders are expected to provide written reasons for loan application rejections. Visit the branch and ask clearly: “Was my application rejected due to data mismatch, CIBIL score, business risk, or something else?” Note down the exact phrases used. You can also check official sources and your rejection letter.

Step 2 – List every mismatch: Compare the rejection feedback against your application form, KYC, bank statements, GST, Udyam and project report. Mark specific inconsistencies – wrong start date, different address, mismatched turnover.

Step 3 – Correct source records first: If Aadhaar has wrong spelling or Udyam has outdated activity, update those government records before approaching the bank again. Wait until changes reflect in databases.

Step 4 – Revise the project report and application: Rewrite the project report to match corrected data. Fill a fresh mudra loan application carefully. A weak or missing business plan leads to loan application denial, so prepare a basic business plan with realistic projections. You can also appeal a rejected Mudra loan if you believe the rejection was unjust.

Step 5 – Reapply transparently: Disclose that a previous application was rejected due to inconsistencies which have now been corrected. Many applicants apply online or visit the branch directly. Be ready during field inspection to show rental agreements, bills, licences and live business operations. You can approach the same bank or a different one, including institutions where you can submit required Mudra loan documents afresh.

Practical Tips from CA Manish Gugliya to Avoid Future Mudra Loan Rejections

Drawing from over 20 years of MSME finance experience, here are habits that consistently help get a mudra loan approved:

- Never guess figures like turnover, profit, stock value or monthly sales. Base every number on bank statements, GST returns or ITR. Banks assess and verify these, and any discrepancy is a red flag.

- Use a “master data sheet” with your exact name, address, business description, registration numbers and standard signature format. Copy from this sheet into every form to maintain consistency.

- Avoid common shortcuts: do not copy old project reports from another business, use internet templates with sample data, or apply for the maximum allowed amount without realistic repayment capacity. Changing your stated business activity just to qualify for popular Mudra loan categories is equally risky. Mudra loans are for non-farm, non-corporate activities and do not cover allied agricultural activities.

- Keep all documents updated annually – KYC, shop licence renewals, Udyam, GST principal place of business, bank KYC. When you finally need a business loan, your paperwork will naturally match.

- For loans above ₹5 lakh, invest in professional review of your project report and CMA data. The cost is far lower than losing an opportunity to a wrongly rejected application. Meeting the eligibility criteria is necessary, but consistency across your evidence and proof is what earns approval and gets money disbursed.

Frequently Asked Questions About Mudra Loan Rejection Due to Incorrect Information

Can a single spelling mistake in my name really cause Mudra loan rejection?

A small spelling mistake alone may not cause automatic rejection, but if the variation makes the bank doubt whether Aadhaar, PAN, cibil report and bank account belong to the same person, the banker may reject the application. Ensure your name, father’s name and date of birth are identical across all ID proofs. If variations already exist, submit a written clarification with supporting documents like a Gazette notification or affidavit.

If my address changed recently, will the old address on Aadhaar or GST create a problem?

A recent change of address is common, but not updating Aadhaar, GST or bank KYC while using the new address in the mudra loan application creates an address mismatch. Either update your records before applying or provide both old and new addresses with proof such as a rent agreement and recent electricity bill so the banker understands the transition.

Does a rejection due to inconsistent information affect my CIBIL score?

Simple rejection at the initial appraisal stage normally does not reduce your CIBIL score because no loan was disbursed and no default occurred. However, repeated enquiries for multiple loans within a short period may appear on your credit report and be viewed negatively. Fix your documentation first, then apply once with a complete, well-prepared application.

Can I apply for a Mudra loan with another bank after being rejected due to data mismatch?

Yes, you can approach another bank or financial institution. However, if you do not correct the underlying inconsistencies, the second lender is also likely to reject the application for the same reasons. Update your KYC and business documents, correct the project report, and be prepared to explain honestly that the earlier rejection has been rectified. This builds trust with the new banker.

Is it necessary to hire a professional like a CA to fix my Mudra loan application errors?

Many micro entrepreneurs can correct simple issues – like address mismatch, wrong mobile number or minor turnover errors – by themselves using the checklists in this article. Professional help from a CA or MSME consultant becomes especially valuable when the loan amount is higher (above ₹5 lakh), when multiple documents need alignment, or when the bank has raised complex queries about business viability, project report or CMA data.

About the Author

CA Manish Gugliya is a Chartered Accountant and MSME Business Consultant with over 20 years of experience helping entrepreneurs prepare Mudra Loan Project Reports, CMA Data, Business Plans, Startup Documentation, Business Valuation Reports, and financial projections. Through Project Report Bank, he shares practical, experience-based guidance to help businesses understand banking requirements and improve their chances of successful loan approval.

- How to Identify the Actual Reason Behind Your Mudra Loan Rejection

- How Banks Assess Mudra Loan 2026 Risk Before Rejecting an Application

- Mudra Loan Interview Rejected: Common Mistakes and How to Prepare Successfully (2026 Guide)

- Mudra Loan Rejected Because the Proposed Business 2026 Already Has High Local Competition

- Mudra Loan Rejected Because Business Category Is Outside Bank Lending Preference 2026

- Mudra Loan Rejected Because of Inconsistent Information in the Application 2026 – Common Mistakes & How to Fix Them

- Mudra Loan Rejected Due to Doubts About Business Continuity – Why Banks Lose Confidence & How To Avoid It (2026 Guide)

- Mudra Loan Rejected After Site Inspection 2026 – What Banks Usually Observe

- Mudra Loan Rejected Because Previous Loan Was Declined (2026 Guide by CA Manish Gugliya)

- Mudra Loan Rejected Due to Multiple Risk Factors – How Banks Decide (2026 Complete Guide)

- Mudra Loan Rejected Because Loan Purpose Not Eligible – Expert Guide by CA Manish Gugliya (2026)

- Mudra Loan Rejected Because the Proposed Business Is Not Viable 2026

- Mudra Loan Rejected Due to Business Type 2026 – Practical Guide by a CA

- Mudra Loan Rejected Despite Meeting Eligibility – Why It Happens & What You Can Do (Guide by CA Manish Gugliya)

- How to Improve Your Chances of Mudra Loan Approval