Disabled persons can apply for a Mudra loan for disabled persons under the Pradhan Mantri MUDRA Yojana (PMMY). This scheme offers financial assistance to support entrepreneurship among disabled individuals. In this article, we will discuss the eligibility criteria, benefits, application process, and success stories of physically disabled entrepreneurs.

Key Takeaways

- The Mudra Loan Scheme under the Pradhan Mantri MUDRA Yojana provides accessible financial assistance to disabled persons, promoting entrepreneurship and financial inclusion.

- Eligibility for Mudra loans for disabled individuals is based on the viability of a business plan rather than physical ability, ensuring equal access to funding.

- The scheme offers three categories of loans (Shishu, Kishor, and Tarun) catering to various business stages, with interest rates varying by bank and no collateral required.

Introduction

The Mudra Loan Scheme, part of the Pradhan Mantri MUDRA Yojana (PMMY), is a government initiative aimed at supporting small businesses and micro enterprises through accessible financial assistance. The scheme recognizes the importance of promoting entrepreneurship among various income groups, including Persons with Disabilities (PwDs), ensuring that everyone has the opportunity to build a sustainable livelihood.

Promoting entrepreneurship among PwDs is not just a matter of economic inclusion but also a step towards empowering individuals to lead independent and fulfilling lives. The government aims to bridge the gap and create equal opportunities by offering financial support and promoting financial inclusion.

A business loan for disabled persons in India under the Mudra scheme helps individuals start small businesses like retail shops, service units, or online work without requiring collateral.

If you want to understand basic eligibility, you can also read our detailed guide on Mudra loan without CIBIL score.

Understanding Mudra Loans for Disabled Persons

Designed to assist small and micro businesses, the Mudra Loan Scheme under the Pradhan Mantri MUDRA Yojana (PMMY) offers accessible financial support. This initiative is especially beneficial for disabled persons, acknowledging the unique challenges they face in entrepreneurship. The scheme’s primary objective is to promote entrepreneurship among various income groups while enabling easy access to financing, thereby reducing the financial burden on aspiring entrepreneurs through micro units development.

Mudra loans support small, self-employment-oriented businesses for disabled persons, allowing them to overcome financial barriers and achieve their entrepreneurial dreams. The scheme ensures financial assistance is within reach for those who need it most by tailoring business loans to the needs of disabled people.

A business loan for disabled persons in India under the Mudra scheme helps individuals start small businesses like retail shops, service units, or online work without requiring collateral.

Why This Scheme Matters for Physically Disabled Entrepreneurs

Challenges Faced by Physically Disabled Entrepreneurs:

Physically disabled entrepreneurs often encounter significant obstacles such as limited access to capital, societal biases, and physical barriers, which can hinder their ability to achieve financial independence and pursue entrepreneurial goals.

Government Inclusion Efforts:

State government initiatives, including schemes like Stand-Up India and Mudra, aim to tackle these challenges by providing necessary support and resources to disabled entrepreneurs.

Financial Assistance through Mudra Loan Scheme:

The Mudra Loan Scheme is crucial as it offers financial assistance specifically for small, self-employment-oriented businesses run by disabled persons, helping to reduce the burden of initial capital costs.

Empowerment and Inclusivity:

Beyond just financial aid, the scheme empowers disabled entrepreneurs by addressing their unique needs, fostering a more inclusive and equitable business environment.

Promoting Equal Opportunity:

This approach ensures that everyone, regardless of physical ability, has the chance to succeed and contribute meaningfully to the economy.

Eligibility Criteria for Physically Disabled Applicants

Eligibility criteria for a Mudra loan include:

- Applicants must be Indian citizen.

- Generally, applicants should be between 18 and 55 years old.

- There are no specific age restrictions for physically disabled individuals.

- The key deciding factor is the viability of the business plan rather than the physical ability of the applicant.

Physically disabled entrepreneurs are just as eligible for Mudra loans as any other citizen, ensuring that disability does not hinder access to funding. Applicants must present a viable business plan demonstrating potential for success. This ensures the focus remains on the business’s potential rather than the entrepreneur’s physical abilities.

Many applicants also ask whether PAN or GST is required. You can check our guide on Mudra loan without PAN card.

Types of Mudra Loans Available to Disabled Persons

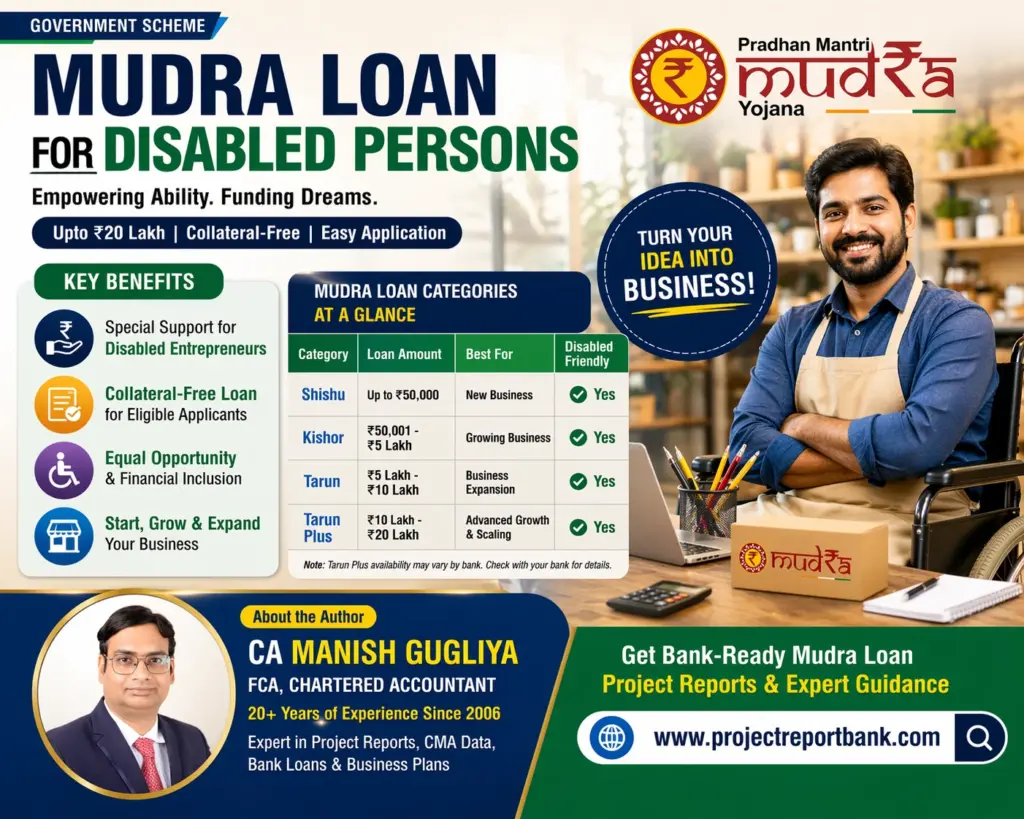

The Mudra Loan Scheme offers three distinct categories designed to cater to various financial needs: Shishu, Kishor, and Tarun. Each category addresses different stages of business development, providing appropriate financial assistance based on the scale and requirements of the business. The maximum loan amount available under this scheme can go up to ₹10,00,000, making it suitable for a wide range of business activities.

Mudra loans cater to various purposes, such as working capital, purchasing commercial vehicles, and investing in machinery. This flexibility ensures that entrepreneurs can use the funds in a way that best supports their business goals.

The following sections delve into each loan category:

| Category | Loan Amount | Best For | Disabled Friendly |

|---|---|---|---|

| Shishu | Up to ₹50,000 | Starting a new small business | ✔ Yes |

| Kishor | ₹50,001 – ₹5 lakh | Growing or stabilizing business | ✔ Yes |

| Tarun | ₹5 lakh – ₹10 lakh | Expanding an existing business | ✔ Yes |

| Tarun Plus | ₹10 lakh – ₹20 lakh | Advanced expansion & scaling | ✔ Yes |

Shishu Category

The Shishu category offers financial support for small ventures, with a cap of ₹50,000, ideal for entrepreneurs needing initial funding to launch their business.

Shishu loans cater to various small enterprises business activities, offering the essential first step for budding entrepreneurs.

Kishor Category

The Kishor category supports business expansion, catering to medium growth needs with loans ranging from ₹50,001 to ₹5 lakh, suitable for businesses past the initial stage looking to expand.

This category aids in scaling up businesses and meeting medium-term financial needs.

Tarun Category

The Tarun category caters to established businesses seeking further growth. Loans in this category range from ₹5 lakh to ₹10 lakh, offering substantial funding for operational businesses aiming to expand further.

It supports significant business developments and capacity enhancements.

Disabled entrepreneurs can apply under all categories, including Tarun Plus (₹10 lakh to ₹20 lakh), depending on their business growth and funding requirements.

You can explore business ideas suitable for each category in our article on best business ideas under Mudra loan.

Interest Rates and Repayment Tenure

Interest rates for Mudra loans vary by bank and depend on the borrower’s credit profile, with the rate of interest being a crucial factor. Loan tenures can range from 1 to 7 years, based on the lender’s discretion. A significant advantage of Mudra loans is the lack of collateral requirement, making it accessible for physically disabled entrepreneurs without substantial assets to pledge.

Physically disabled applicants could receive an interest subsidy under the National Handicapped Finance and Development Corporation (NHFDC). Additionally, there is priority lending for physically disabled applicants under certain bank Corporate Social Responsibility (CSR) or social inclusion initiatives. This ensures disabled entrepreneurs have a better chance of accessing funds without undue delays.

Required Documents for Mudra Loan Application

Applicants must provide several documents to validate their identity and business viability, including a government-issued photo ID, proof of current address, and a Disability Certificate to confirm eligibility. Obtaining Udyam Registration can further enhance the credibility of small businesses applying for Mudra loans.

Other required documents include:

- Aadhar Card

- PAN Card

- Address Proof

- Business plan

- Quotation for machinery

- Bank statement

- Passport-size photos

- Documents required

- Other documents

Having all documents ready and organized streamlines the application process and improves the chances of loan approval.

To apply for a Mudra loan for handicapped persons, it is important to keep all documents ready, including Aadhaar card, PAN card, disability certificate, business plan, and bank statements.

If you want to increase approval chances, read our detailed guide on how to prepare a Mudra loan project report.

Application Process for Physically Disabled Entrepreneurs

Applying for Mudra loans involves several steps:

- Physically disabled entrepreneurs should begin by choosing a suitable lender, such as banks or specialized financial institutions offering Mudra loans.

- Required documents include a Disability Certificate.

- Applicants may need a caregiver to apply on their behalf.

- Eligible borrowers can apply directly through financial institutions or online portals.

The Entrepreneurship Development Institute of India offers training and support tailored for aspiring entrepreneurs with disabilities. This additional support is invaluable for preparing a robust business plan and understanding the application process.

Choosing a Lender

When selecting a lender, applying through banks where you already hold an account is advisable, as they may view you more favorably. Lenders for Mudra loans include both public and private sector banks, regional rural banks, along with specialized financial institutions like Punjab National Bank.

Researching specific Mudra loan schemes and eligibility criteria is crucial for informed decision-making.

Preparing Your Business Plan

A well-structured business plan is crucial for loan approval. It should demonstrate your business understanding, outline fund allocation, and present a clear repayment form strategy.

A comprehensive business plan can significantly improve your chances of getting the loan approved.

Submitting the Application

Organize all application form and supporting documents for clarity and ease of verification. Submit your application to your chosen lender. Ensure all supporting documents are included, whether submitted online or offline.

After submission, the lender will evaluate the information and conduct necessary checks to approve the loan.

Salaried individuals can also apply. Read our guide on Mudra loan for salaried persons.

Success Stories of Physically Disabled Entrepreneurs

Mudra loans have significantly broken barriers for disabled entrepreneurs, proving that physical disabilities do not hinder business aspirations. For instance, M/s Malsawm Handloom generated a profit of Rs. 350,000 during festive seasons, showcasing small business potential.

Inspirational stories like Raju Das Bairagi, who transitioned from a cook to launching his own fast-food business, and Firozkhan Baghban, who established his computer education venture with a Mudra loan of ₹195,000, serve as powerful motivators for other aspiring entrepreneurs.

These success stories highlight the resilience and determination of disabled entrepreneurs.

Additional Support and Resources for Disabled Entrepreneurs

Several organizations offer additional support and resources for disabled entrepreneurs. The National Disabilities Finance and Development Corporation provides funding and support through state agencies. IDEA Saksham and Sarthak Educational Trust offer market linkages, financial support, and employment programs to enhance entrepreneurial capabilities.

Other notable organizations include Samarthanam, focusing on education and vocational training, and the NEDAR Foundation, a virtual incubator for micro-entrepreneurs with disabilities. These resources are invaluable for disabled entrepreneurs looking to establish and grow their businesses.

Tips for Improving Approval Chances

Maintaining consistent and accurate documents across all identification and business records is crucial for avoiding rejections. A comprehensive business plan should clearly outline fund allocation for business development. Regular follow-ups with the bank after submitting your application keep you informed and demonstrate your commitment to the process.

Mentioning any training or experience relevant to your business and seeking support from NGOs or District Industries Centres can also improve approval chances. These steps enhance your credibility and show lenders you are well-prepared and committed to your business venture.

Many applications get rejected due to small mistakes. Check common reasons for Mudra loan rejection and how to fix them.

Combining Mudra Loans with Other Schemes

Entrepreneurs with disabilities can enhance their funding opportunities by integrating Mudra loans with other government initiatives supporting disabled individuals. Programs like the Stand-Up India Scheme can be used alongside Mudra loans, offering additional financial support for starting or expanding a business.

Combining Mudra loans with the Pradhan Mantri Employment Generation Programme (PMEGP) allows disabled entrepreneurs to access higher loan amounts for their business needs. Exploring various state-specific schemes complementing Mudra loans can also provide tailored financial assistance.

Common Questions from Physically Disabled Applicants

Common questions from physically disabled applicants often revolve around:

- Collateral requirements

- Shop or GST registration

- Business experience

- Caregiver applications

A key advantage of Mudra loans is that no collateral security is required, making them accessible for physically disabled entrepreneurs, providing numerous benefits.

Many applicants have the following questions and concerns regarding Mudra loans:

- Whether they need to register their shop or obtain GST registration to apply.

- How previous business experience impacts the success of their application.

- Issues related to caregiver applications and the processes involved.

Encouragement and Final Thoughts

The Mudra Loan Scheme reaffirms that physical disability is not a barrier to entrepreneurial success. The scheme’s financial support and inclusive policies encourage aspiring entrepreneurs to take the leap and pursue their dreams. Sharing success stories and providing detailed information on the application process, this guide aims to inspire and empower disabled persons to realize their business potential.

Take inspiration from those who have walked this path before you. With determination, a solid business plan, and support from schemes like Mudra, you too can build a successful enterprise. Remember, your physical limitations do not define your potential. The Mudra Loan Scheme is here to help turn your entrepreneurial aspirations into reality.

Need Help in Getting Mudra Loan Approved?

If you are planning to apply for a Mudra loan, a professionally prepared project report can increase your approval chances.

At Project Report Bank, we provide:

- Mudra loan project reports

- CMA data for bank loans

- Business plan preparation

Contact us to get your report prepared quickly.

Summary

To summarize, the Mudra Loan Scheme offers a robust financial platform for disabled entrepreneurs to start and grow their businesses. The scheme provides three loan categories—Shishu, Kishor, and Tarun—each catering to different stages of business development. Eligibility criteria are inclusive, focusing on the viability of the business plan rather than physical ability. The process is straightforward, requiring essential documents and a clear business strategy.

By combining Mudra loans with other supportive schemes, physically disabled entrepreneurs can maximize their funding opportunities. Remember to maintain accurate documentation, prepare a comprehensive business plan, and seek additional support from specialized organizations. With these steps, you are well on your way to achieving your entrepreneurial dreams. The journey may be challenging, but the rewards are worth it. Empower yourself with the information and resources available, and take the first step towards your business success.

About the Author

CA Manish Gugliya is a Fellow Chartered Accountant (FCA) with more than 20 years of experience in finance, taxation, and project report preparation. He has been actively practicing since 2006 and has helped hundreds of entrepreneurs, startups, and MSMEs in securing bank loans including Mudra loans.

He specializes in:

- Mudra Loan Project Reports

- CMA Data for Bank Loans

- Business Plan Preparation

- Income Tax & GST Advisory

Through his platform Project Report Bank, he provides ready-to-use and customized project reports that improve loan approval chances for individuals and businesses across India.

With deep practical knowledge of banking requirements and government schemes, CA Manish Gugliya aims to simplify the loan process and empower aspiring entrepreneurs, including disabled persons, to start and grow their businesses.

Can a disabled person apply for Mudra loan in India?

Yes, disabled persons (PwDs) can easily apply for a Mudra loan in India. Banks focus on the business plan and repayment capacity, not on physical ability.

What is the maximum Mudra loan amount for disabled persons?

Disabled persons can get up to ₹10 lakh under the Tarun category and up to ₹20 lakh under Tarun Plus (depending on bank policies and eligibility).

Is Mudra loan available without collateral for disabled applicants?

Yes, Mudra loans are completely collateral-free, making them highly accessible for disabled entrepreneurs who do not have assets to pledge.

What documents are required for Mudra loan for disabled persons?

Key documents include Aadhaar card, PAN card, disability certificate, business plan, bank statement, and quotation for machinery or business setup.

What types of businesses can disabled persons start with Mudra loan?

Disabled persons can start small businesses like retail shops, tailoring units, mobile repair shops, online services, food businesses, and more using Mudra loans.

What is the interest rate on Mudra loan for disabled persons?

Interest rates vary from bank to bank, generally ranging between 8% to 12% depending on the applicant’s credit profile and business viability.

Is GST registration required for Mudra loan approval?

GST registration is not mandatory for all businesses. It depends on the nature and turnover of the business. Small businesses can apply without GST in many cases.

Can a disabled person apply for Mudra loan online?

Yes, disabled persons can apply online through bank websites or portals like Udyamimitra, or visit nearby banks for offline application.

How can a disabled person increase chances of Mudra loan approval

A strong business plan, proper documentation, stable bank transactions, and a well-prepared project report can significantly improve approval chances.

Can Mudra loan be combined with other government schemes for disabled persons?

Yes, Mudra loan can be combined with schemes like PMEGP, Stand-Up India, and NHFDC support programs to get higher financial assistance.